The basics of annual tax filing for startups – due dates and more

If you are a business owner, September 30 and October 30 are two important dates for you. September 30 is the due date for filing the Income Tax Return for your company, whereas October 30 is the due date for filing the annual financial statements with the Registrar of Companies (RoC). They are more crucial if you are a VC/Angel funded startup or looking for such third party investment. A zero non-compliance business environment is the pre-requisite for this.

In the fervour of starting a new business, it’s easy to overlook the long-term impact of a sustainable regulatory decision that extends to recording the initial transactions, filing your tax return and other mandates. In the rush to go to market, it’s easy to think the business model itself will carry the day. Two out of three startups die out in their first three years of operation. While the reason may not be related to tax and regulatory non-compliances, this builds on the cause.

Most startups think that since they have no business transactions or they have incurred losses, they do not need to file their taxes. The reality, however, is every company/Limited Liability Partnership (LLP) has to comply with five basic compliances irrespective of its business situation. They are detailed below:

Accounting and Book Keeping

Recording the transactions and preserving bills and invoices to back financial statements is something that most business owners dread. Avoiding this leads to serious repercussions. For example, at the time of incorporation, a company pays the registration fees, name approval fees and stamp duty to RoC. Further, the promoters of the company also hire a professional firm to guide them through the entire incorporation procedure, which again involves cash outflow.

These expenditures, though pre-incorporation in nature, provides tax-saving benefits to the company, to the extent of one-fifth of such expenses every year. Further, invoices carrying break-ups of VAT and service tax is a boon, as far as claiming credit for both is concerned. The company should keep records of all expenses made specifically for business, since these are deductible against business revenues. Even if the company is suffering losses, it is advisable to maintain records in order to raise the losses and set it off with future profits.

Penalty for Non-Compliance:

In case of non-compliance, persons responsible shall, in respect of each offence, be punishable with imprisonment for a term which may extend to one year or with fine which shall not be less than Rs. 50,000 but which may extend to Rs. 5,00,000 or both in case of companies.

Income Tax Return Filing

Filing of income tax return is the most authentic proof of the income earned as all are required to file it. But many do not file tax returns as they are unaware of the procedure. Startups should appoint a tax consultant who will help them avail the benefits of filing tax return in time. Some of the benefits include:

- Filing timely returns saves one from the assessments of income by the income tax officials.

- A business having losses can carry it forward and get it set-off with future profits.

- For making an investment, filing income tax return on time is essential.

- Tax refunds can be claimed only when income tax return is filed.

The due date for filing this return is September 30 each year. However, if transfer pricing provisions are applicable for your business, this due date changes to November 30 each year.

Penalty for Non-Compliance:

Late filing of return will attract interest u/s 234A i.e. if the assessee fails to file income tax return within the time prescribed by Section 139, he shall be liable to pay interest at one per cent per month or part of the month from the due date of filing of return to the actual date of filing of its return. A further penalty can be levied up to Rs. 5,000 for non-filing of tax returns us 271F.

However, for the purpose of filing income tax filings, the year has to close on March 31 each year. For that purpose, you only need to file a simple format of Profit and Loss Account and Balance Sheet with the department and then prepare the return and file it within the prescribed due date.

Statutory Audit Compliances

Companies are mandatorily required to get their accounts audited annually whereas only those LLPs having a turnover of more than Rs 40 lakh or Rs 25 lakh contribution in any financial year are required to get their accounts audited annually as per the LLP Act.

The LLP Act provides that the partners of such LLP if decided not to get audit of the accounts of the LLP then such LLP shall include in the Statement of Account and Solvency a statement by the partners to the effect that the partners acknowledge their responsibilities for complying with the requirements of the Act and the Rules with respect to preparation of books of account and a certificate in the Form 8. However no such relaxation is provided to companies.

ROC Compliances

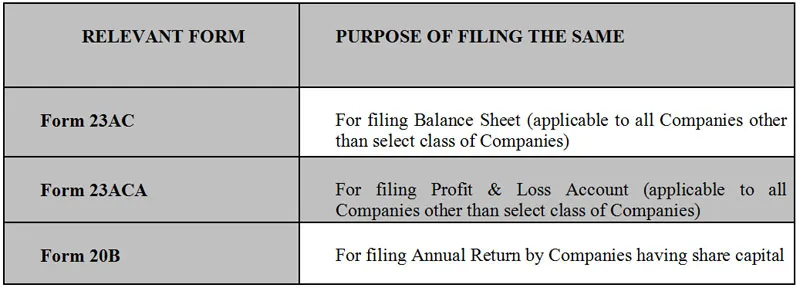

Every company (having or not having share capital) and LLP has to file its financial reports with the Ministry of Corporate Affairs annually. It constitutes a component of ‘Annual RoC Filing’ mandated by Companies Act, 2013. As a part of annual filing, Companies incorporated under the Companies Act 2013, are required to file the following e-forms with the RoC:

Penal Provisions:

The penal provisions of RoC are so stringent that companies have been shut down due to this. The additional fees can be as high as upto 12 times of normal fees. Further, there also provisions where huge penalties are laid per day on officers as well as the companies simultaneously. Companies Act 2013 also has provisions of hard crust penalties like imprisonment of company directors on grounds of severe non-compliance.

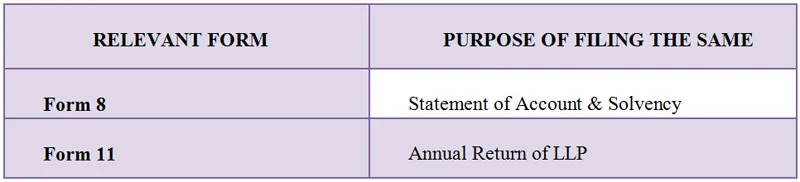

As a part of Annual Filing, LLPs are required to file the following e-forms with the RoC:

Penal Provisions for Limited Liability Companies –

Surprisingly, there are no slabs for late filing fee for LLPs. In this regard, the straight rule of computation of late filing fee is Rs 100 per day of delay in filing. The number of days of delay in filing is calculated from the due date of filing to the actual filing date.

As mentioned earlier, these compliances have to be adhered to irrespective of your business situation. Non-compliance of these provisions has the capacity to shut down a full-fledged business. If you still have not started working on this, we suggest you buck up. You still have 21 days at hand!

You may get in touch with the author on his website Taxmantra.com and get more information.