Swiggy's quick commerce profit margins hurt as expansion, discounts take precedence

While Swiggy saw improvement in its core food delivery business, its quick commerce arm witnessed lower margins as dark store, expansion, customer acquisition and retention costs were driven up due to competition.

Food delivery player Swiggy's executives reasoned that the worsening contribution margins of its quick commerce arm, Instamart, was due to its focus on store expansion.

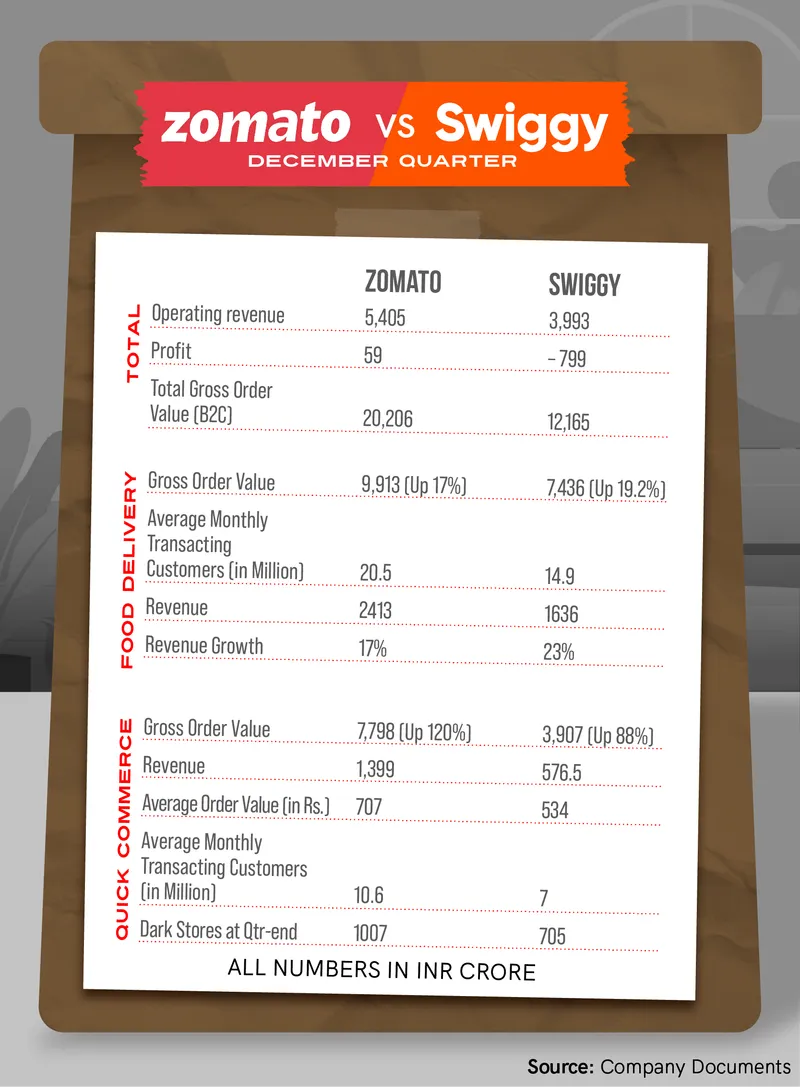

The company saw its contribution margins, a metric for profitability, dip to -4.6% in Q3 from -1.9% in the quarter ended September 2024. During the same period, its adjusted EBITDA margins also contracted to -14.8% in Q3 from -10.6% in the previous quarter.

Swiggy is focused on increasing its store density, penetration across pin codes, competition-fueled discounting, and customer acquisition costs. It is also transitioning its existing stores into larger formats and Megopods to expand the scope of serviceable categories and add more monetisable SKUs.

"It's also fair to assume that a lot of growth from here on store addition is going to be to manage the overall category growth and not necessarily entering into newer areas," said Rahul Bothra, CFO at Swiggy, in a post-earnings call with the analysts.

Company executives expect the competition in the quick commerce space to remain heated until the foreseeable future as it witnesses a growing share from categories beyond groceries. Contribution from non-grocery categories to the overall GOV has improved to 14% from 3.5% on a year-on-year (YoY) basis.

This comes as newer players, vertical marketplaces as well D2C brands are trying to reach consumers faster through in-house delivery formats or alternative quick commerce offerings.

Quick commerce market leader Blinkit's parent Zomato, in its third-quarter earnings, also saw its previously profitable quick commerce arm slipping back into the red after pulling forward growth investments in the unit. It added about 216 stores during the third quarter, while Swiggy added about 96 net new dark stores on top of expanding the size of its existing stores. Blinkit also saw its contribution margins dip from 3.8% in second quarter to 3% in third quarter.

Swiggy managed to bump up its monthly transacting users to 7 million and average order value to Rs 534, as compared to Zomato's 10.6 million and Rs 707, respectively.

"So, we are slightly behind the curve from that perspective in terms of maturity of stores and the profitability profile, which is led by some of the average order value line as well as the advertising revenues, which have started to move up meaningfully," says Bohra.

However, Swiggy's expansion has yet to translate to significant growth in order frequency. During the quarter, its order frequency per dark store was at 1,129 and grew just 6% sequentially, and about 14% YoY.

"One of the things that we saw was the store expansion was also a bit essentially back-ended," said Amitesh Jha, CEO at Swiggy Instamart, in the post-earnings call.

"What essentially happens is when you acquire a customer, their orders won't increase immediately. If the store expansion is a bit back-ended, new customers are going to come essentially later in the quarter. Our growth is related to—what is the percentage of new customers that we are essentially having. If those percentages are higher, it will lead to a lower order frequency as well," he explained.

Improvements in food delivery

Swiggy saw significant improvements in adjusted EBITDA margins of its food delivery business, from 1.6% in September quarter to 2.5% in Q3, further fueling its 5% guidance in the medium term.

Swiggy attributes the improvements to innovation in terms of offerings like the 10-minute food delivery service Bolt, which already accounts for about 9% of all its orders. It has also seen higher advertising revenue from its self-service advertising tool.

"If Bolt grows from here, which we expect it to, we do continue to see our margins expand both on the contribution side and operating leverage kicking in through EBITDA," said Rohit Kapoor, CEO-Food Marketplace, Swiggy on the scope for margin dilution with time-intensive offerings like Bolt.

Swiggy's core food delivery business, registering a topline of Rs 1,636 crore, saw a marginal growth of 3.7% from the previous quarter, hurt by a broad-based demand slowdown. On a year-on-year basis, this growth was more than 23%.

On a consolidated level, the foodtech company's losses widened to Rs 799 crore from Rs 574 crore in the previous year. It clocked a 30% YoY growth in operating revenue to Rs 3,993 crore in the quarter ended December 2024, up from Rs 3,048 crore earned in the corresponding quarter last year, according to an exchange filing. However, the company expects to be on track for its positive adjusted EBITDA timeline on a consolidated level by the October-December 2025 quarter.

Edited by Kanishk Singh